UPI’s Growth Trajectory: Revolutionizing Digital Payments

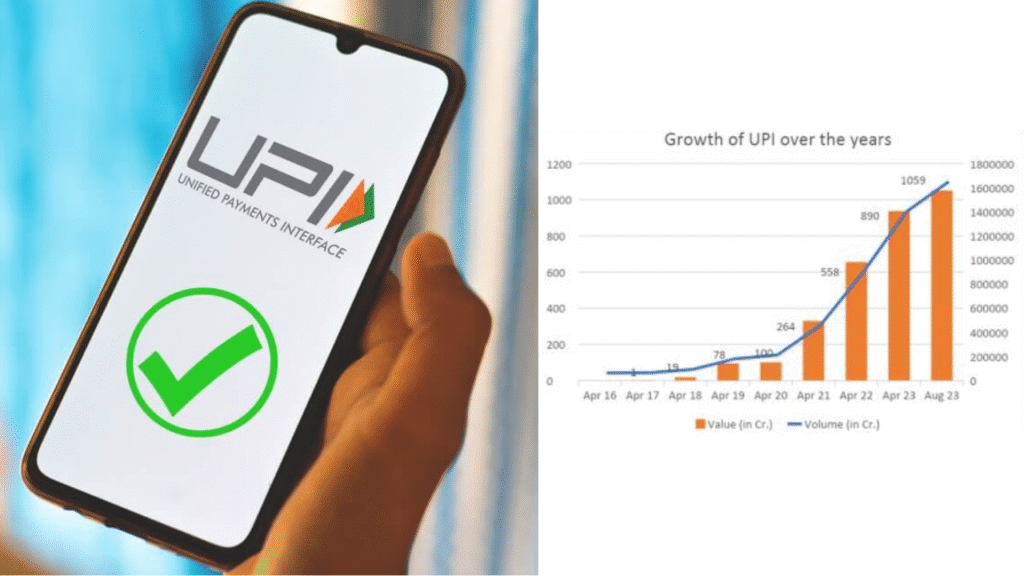

MUMBAI — From bustling street markets in Delhi to quiet village shops in Tamil Nadu, India’s Unified Payments Interface (UPI) has become the heartbeat of the nation’s digital economy. In 2024, UPI processed a staggering 144.78 billion transactions worth ₹217.33 trillion, a 71% volume jump from 2023, cementing India’s place as a global leader in real-time payments. Fueled by widespread smartphone use, government backing, and a knack for simplicity, UPI’s growth is reshaping how money moves, though challenges like fraud and rural connectivity gaps keep the journey bumpy.

The numbers are jaw-dropping. By October 2024, UPI handled 16.58 billion transactions in a single month, up 53% from the previous year, with a value of ₹24.09 trillion, per the National Payments Corporation of India (NPCI). Apps like PhonePe, Google Pay, and Paytm dominate, processing 88% of transactions, while small merchants and kirana stores now accept QR code payments as easily as cash. “UPI’s changed everything,” said Anil Sharma, a tea stall owner in Kolkata. “Customers pay with a scan, and I don’t worry about change.”

What’s driving this boom? With 1.2 billion mobile connections and 700 million internet users, India’s digital infrastructure is a powerhouse. Government schemes like Digital India and Jan Dhan Yojana, which opened 540 million bank accounts, have brought millions online. UPI’s zero-fee model for small transactions and instant transfers make it a hit, even for daily wagers like Sunita Devi in Bihar, who sends ₹500 home via UPI. “It’s fast, and I don’t need a bank visit,” she said. The Reserve Bank of India’s push for interoperability—linking UPI with RuPay credit cards—has further boosted its reach.

Businesses are cashing in. E-commerce sales spiked 22% in 2024, with UPI driving 80% of online payments, per Razorpay data. Small businesses, from food carts to salons, report 30% higher sales since adopting UPI, as customers spend more freely. “My salon’s gone cashless,” said Priya Menon, a Bengaluru entrepreneur. “UPI’s quick, and clients love it.” Globally, UPI’s catching eyes—Singapore, UAE, and France now support cross-border UPI payments, with remittances from NRIs up 15%.

But it’s not all smooth. Cyberfraud surged, with ₹1,750 crore lost to UPI scams in 2024, per NPCI. Phishing and fake QR codes are rising threats, hitting small merchants hardest. “I lost ₹10,000 to a scam,” said Rajesh Yadav, a shopkeeper in Lucknow. Rural areas, with only 40% reliable internet, also lag, leaving 300 million potential users offline. The NPCI’s cap on third-party apps handling 30% of transactions has sparked debates, with giants like PhonePe pushing back.

For India’s economy, UPI’s a game-changer, contributing 3% to GDP growth by cutting cash-handling costs and boosting financial inclusion. The survey notes digital payments saved ₹2 trillion in transaction costs in FY24. Fintech startups are thriving, with investments hitting $2.5 billion in 2024. But scaling up means tackling fraud and bridging the digital divide.

Looking ahead, UPI’s set to soar. NPCI aims for 1 billion daily transactions by 2027, with plans to expand to 20 countries. The RBI’s UPI Lite for low-value offline payments could bring rural users onboard. “UPI’s just getting started,” said Sanjay Patel, a fintech analyst in Mumbai. For businesses and everyday Indians, it’s more than a payment tool—it’s a ticket to a cashless future. As UPI rewrites how money moves, India’s digital economy is charging forward, one tap at a time.